![[HERO] Does a 6% Mortgage Rate Really Matter in 2026?](https://bexleyrealtygroup.com/wp-content/uploads/2026/04/AxIADEp4lE_-1024x675.webp)

Does a 6% Mortgage Rate Really Matter in 2026?

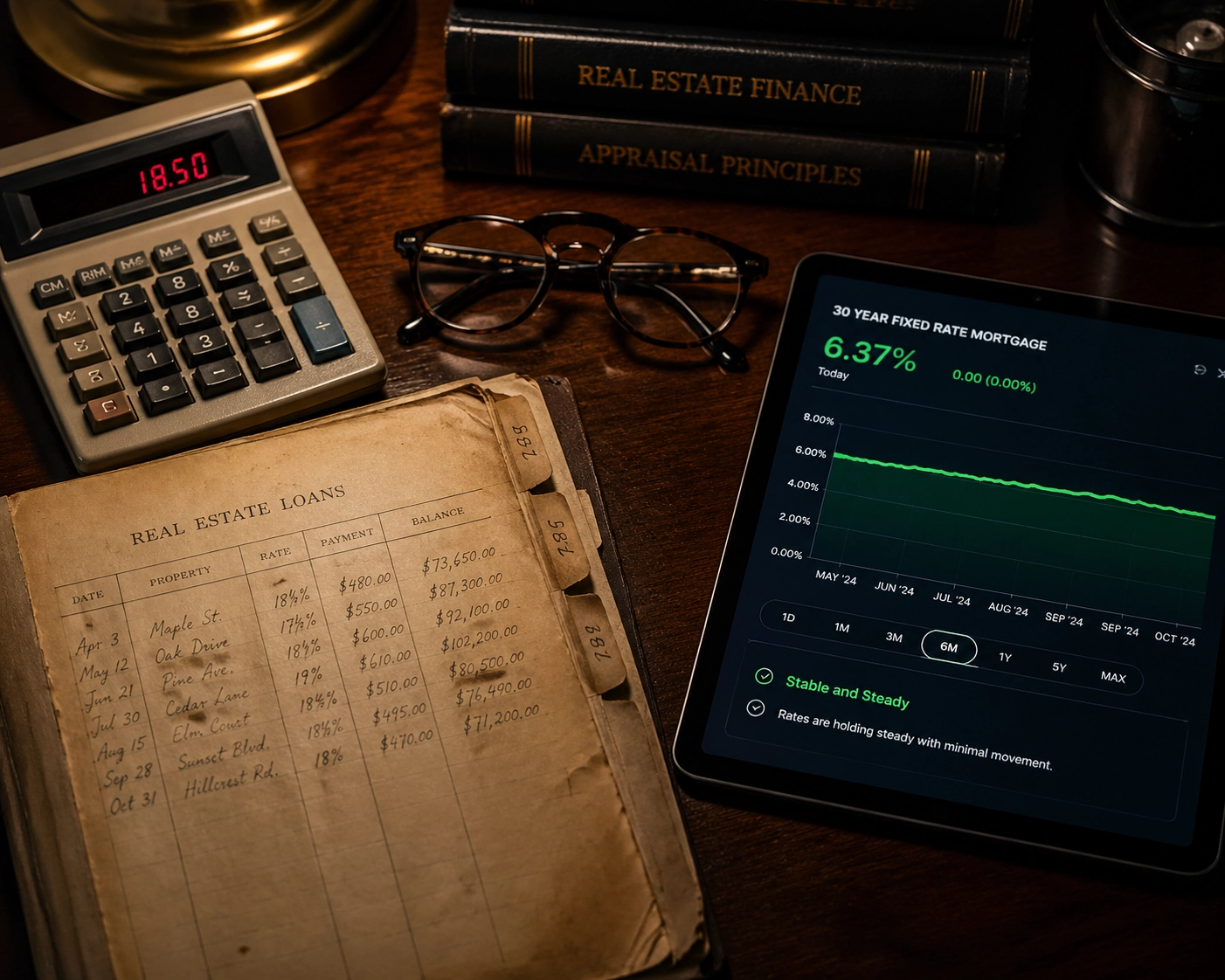

Let’s be honest: back in 2021, we were spoiled. We lived through a period of interest rates so low they felt like a clerical error. But here we are in April 2026, and the dust has finally settled. The Federal Reserve has stopped its frantic dancing, and the mortgage market has found its “new normal” at around 6%.

For some, 6% feels like a punch in the gut compared to the 3% “glory days.” But for the savvy Houston homebuyer, the question isn’t “Why aren’t rates 3%?” The question is “Why am I still sitting on the sidelines while my future home gets more expensive every day?”

If you’re still holding out for a return to pandemic-era rates, I have some tough love for you: that ship hasn’t just sailed; it’s been decommissioned and turned into a floating museum. Waiting for 3% in 2026 is like waiting for gas to be $0.99 again, it makes for a great story, but it’s a terrible financial strategy.

The “Waiting for 3%” Trap

We see it all the time at Bexley Realty Group. A buyer finds a home they love in Katy or The Heights, looks at the monthly payment, and says, “I’ll wait until rates drop to 4%.”

Spoiler alert: while you wait for a 1% or 2% drop in interest rates, the price of the home is busy doing its own thing, climbing. In a market as resilient as Houston, home price appreciation often outpaces the savings you’d get from a slightly lower interest rate. If a $400,000 home appreciates by 5% in a year, it’s now a $420,000 home. Even if the rate drops by half a point during that year, you’re now financing a larger amount at a higher purchase price. You’ve “saved” on interest but lost on equity.

The Math: Appreciation vs. Interest Cost

Let’s look at the numbers because the math doesn’t lie. If you buy a home today at 6%, you are locking in today’s price. In Houston, we’ve seen the market remain steady even through national turbulence, as highlighted in our previous reports on the Houston housing market.

Imagine you buy a home for $450,000 with a 6% rate.If you wait 12 months and the home price increases to $475,000 (a modest 5.5% jump), but the rate miraculously drops to 5%, your monthly principal and interest payment might look similar. However, you just missed out on $25,000 in pure equity. That’s $25,000 of wealth you didn’t build because you were chasing a percentage point.

Furthermore, we’ve seen families make the move and find success regardless of the national narrative. Take a look at how the Martinez family found their dream home despite the shifting landscape. They prioritized the home over the rate, and in 2026, they’re sitting on significant equity while others are still refreshing mortgage news sites.

6% is Actually Historically “Cheap”

If you talk to anyone who bought a home in the 1980s, they will happily tell you about their 18% mortgage while they walked uphill both ways to school. In the 1990s, an 8% rate was considered a “steal.”

Historically, the average 30-year fixed mortgage rate in the United States has hovered around 7.7%. In that context, 6% is actually below average. We just became addicted to the “free money” era of 2020-2022. That era was an anomaly, a black swan event triggered by a global crisis. It wasn’t the standard; it was the exception.

By accepting that 6% is a fair, stable, and historically strong rate, you free yourself to focus on what actually matters: the neighborhood, the school district, and the layout of your kitchen.

The “Marry the House, Date the Rate” Strategy

This phrase has been beaten to death by real estate agents, but that’s because it’s fundamentally true. Your purchase price is permanent. Your interest rate is not.

If you buy now at 6% and rates eventually drop to 5% or 4.5% in 2027 or 2028, you can refinance. You get the lower rate and you keep the lower purchase price from 2026. If rates go up to 7% or 8%? You look like a genius for locking in 6%.

This is especially relevant for First-Time Buyers. Getting your foot in the door is the hardest part. Once you own the asset, you are protected against rising rents and you are finally on the “wealth-building” side of the equation. We’ve seen single-family rentals hit record territory in the past, and as a tenant, you get 0% of that appreciation. As an owner, you get all of it.

Why Houston is the Place to Be in 2026

The Houston market isn’t like the rest of the country. We have a diverse economy, a massive medical center, and a port that keeps the engine humming. While other cities might see stagnation, Houston’s inventory has continued to bloom and adapt.

Whether you are looking at new construction in Cypress or a historic bungalow in the Heights, the demand in Houston remains high because people want to live here. This demand acts as a floor for home prices. Even if rates stay at 6% for the next five years, the lack of inventory relative to our population growth means prices are likely to trend upward.

Stop Overthinking the Fed

It is easy to get caught up in what the Federal Reserve is doing or what the latest inflation report says. But your life doesn’t happen in a spreadsheet at the Fed. It happens in your living room.

If you need more space for a growing family, if you’re tired of paying a landlord’s mortgage, or if you’re relocating for a dream job, the 1% difference in a mortgage rate shouldn’t be the thing that stops your life from moving forward.

The Reality Check:

- 3% is gone: It’s time to move on.

- Appreciation is real: You pay for the delay in the form of a higher sales price.

- Refinancing is an option: You aren’t stuck with 6% forever if the market dips.

- Houston is resilient: Our local market holds value better than most.

Summary: Does 6% Matter?

Does a 6% mortgage rate matter? Sure, it matters for your monthly budget and your purchasing power. But it shouldn’t be a dealbreaker. In the grand scheme of real estate history, 6% is a solid, middle-of-the-road rate that allows for a healthy, balanced market. It’s high enough to keep the “insane” bidding wars at bay, but low enough to remain affordable for most working families.

At Bexley Realty Group, we specialize in navigating these exact market conditions. We don’t just find you a house; we help you understand the long-term financial implications of your investment. Whether you are a seasoned investor or a nervous first-time buyer, we are here to provide the clarity you need.

Ready to stop waiting and start owning?

If you want to discuss your specific situation, look at current inventory, or just run the numbers on a specific Houston neighborhood, we’re ready to help.

- Explore our latest listings: BexleyRealtyGroup.com

- Talk to an Expert: Call us directly at 832-648-2492

- Need a consultation? Contact Us today.

Don’t let the “ghost of 3%” haunt your financial future. 2026 is a great year to buy a home in Houston: if you’re brave enough to ignore the noise.

#HoustonRealEstate #MortgageRates2026 #BexleyRealtyGroup #HoustonHomeBuyers #RealEstateTips #KatyTX #HoustonHousingMarket